Cash

Cash is a necessary asset of every company. Additionally, many companies have cash equivalents short-term, highly liquid investment assets meeting two criteria: (1) readily convertible to a known cash amount and (2) sufficiently close to their due date so that their market value is not sensitive to interest rate changes. Only investments purchased within three months of their due date usually satisfy these criteria. Both cash and cash equivalents are classified as cash on the balance sheet and is always a current asset.

Cash and cash equivalents are called liquid assets which mean they are readily available to settle current debts. A company needs liquid assets to effectively operate.

Cash includes physical currency, deposit in bank accounts, checking accounts (demand deposits), and savings accounts (time deposits) as well as customer checks, cashier’s checks, certified checks, and money orders.

Cash Over and Short.

Differences between the count of the cash in a cash register and the record from the register of cash receipts yield cash over and short journal entries. Cash Over and Short is an income statement account recording the income effects of cash overages and cash shortages. Cash Over and Short account usually is combined with other miscellaneous expenses on the income statement.

To record cash over and short, follow these simple rules:

- Record the cash count as a debit to Cash (Physically how much cash the company has)

- Record the cash register record as a credit to Sales (Theoretically how much cash the company should have from the cash register report)

- The difference will be either a debit or a credit to Cash Over and Short

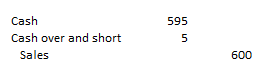

If a cash register’s record shows $600 should be in the register but the cash count from the register is $595, the journal entry is:

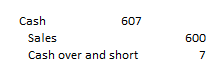

If a cash register’s record shows $600 should be in the register but the cash count from the register is $607, the journal entry is:

Bank Basics

A bank account is a record set up by a bank for a customer. The bank provides a depositor with checks that are serially numbered and imprinted with the name and address of both the depositor and bank. Both checks and deposit tickets are imprinted with identification codes in magnetic ink for computer processing. Electronic funds transfer (EFT) is the electronic transfer of cash from one party to another. No paper documents are necessary.

Bank Statement

Once a month, the bank sends the company its bank statement showing the activity in the account which typically includes:

- Beginning-of-period balance of the depositor’s account.

- Checks and other debits decreasing the account during the period.

- Deposits and other credits increasing the account during the period.

- End-of-period balance of the depositor’s account.

For a bank, a depositor’s account is a liability to the bank. The money belongs to the depositor, not to the bank. When a bank customer makes a deposit or has another type of increase to the account such as interest revenue, the bank records it with a credit or credit memo to the account. When a bank customer’s check decreases the account balance or another type of account decrease takes place such as a bank fee, the bank records it with a debit or debit memo to the account.

The checks the bank has paid on behalf of the bank customer are deducted from the customer’s account. Other deductions that can appear on a bank statement include (1) service charges and fees assessed by the bank, (2) NSF checks (deposited checks which are uncollectible) (3) Errors (rare), (4) withdrawals through automated teller machines (ATMs), and (5) periodic payments arranged in advance by a depositor.

Transactions that increase the depositor’s account include amounts the bank collects on behalf of the depositor, interest earned by the bank customer, and the corrections of previous errors (rare).